Are you dropping sleep over your investments? Implementing a portfolio rebalancing technique is a superb option to give your self some peace of thoughts (and some extra hours of shut-eye each night time). On this article, we’ll define three indicators that point out you must rebalance your portfolio—whereas maintaining feelings out of the equation. We’ll additionally reply the query, “How typically must you rebalance your portfolio?” and discover 5 tax-advantaged financial savings accounts so you possibly can select which choices are one of the best match in your distinctive wealth administration technique.

Do you are feeling overwhelmed by all of the funding choices and techniques in the marketplace immediately? Schedule a name with Bay Level Wealth to learn the way we will help you overcome these obstacles and begin producing returns.

How typically must you rebalance your portfolio?

You need to usually rebalance your portfolio each quarter to yearly. Whichever technique you select, rebalancing works most successfully while you set guidelines for your self and follow them. Consistency will make it easier to rebalance on the proper time.

Nevertheless, these are three extra particular indicators to observe for that point out you must rebalance:

1. When the market goes up or down.

You possible keep in mind that the inventory market took a nosedive when the COVID-19 pandemic hit. At Bay Level Wealth, our rebalancing technique at the moment concerned encouraging our shoppers to make use of this chance to purchase shares at a lower cost, not as a result of we have been making an attempt to time the market, however as a result of the fairness portion of the portfolio went down and our rebalancing technique prompt we purchase. This effort took a robust abdomen to implement. For those who didn’t have money to make use of to buy equities, it required promoting safer, mounted earnings (bonds) and shopping for riskier equities (shares). The important thing in conditions like that is to keep away from slipping into panic mode and follow your technique.

You’ll be able to resolve to rebalance based mostly on whether or not a selected asset class goes up or down by at the least 5 to twenty%. Setting these sorts of parameters holds you accountable to analytics fairly than emotion. That being stated, bear in mind to contact your monetary advisor any time you expertise a serious occasion in your life that might change your monetary state of affairs.

2. While you obtain (or spend) a big sum of cash.

For those who all of the sudden come into extra cash resembling an inheritance or a big bonus, you need to use these funds to rebalance your portfolio. That is typically preferrred as it would mean you can rebalance with out having to promote shares and acknowledge taxable positive factors. Equally, if you should take cash out of your investments, that is additionally a possibility for portfolio rebalancing.

3. While you expertise an enormous life change.

Milestones in life like shopping for a house, having a toddler, or coming into retirement typically sign that it’s a good suggestion to rebalance your portfolio as a result of your earnings, in addition to your monetary wants, might have modified.

Professional Tip: Even when your portfolio comprises solely shares, you’ll nonetheless need to take into account rebalancing it every now and then. A diversified portfolio ought to embrace numerous asset courses, resembling giant and small cap shares. These asset courses carry out otherwise, so you must often modify the quantity of every inside your portfolio. Returning to the instance of the pandemic, giant cap know-how shares carried out properly throughout this time, whereas small cap shares didn’t fare as positively. We bought the upper performers and bought the decrease performers as a part of our rebalancing technique.

Why is portfolio rebalancing essential?

The Greek thinker Heraclitus stated, “The one fixed in life is change.” The identical holds true for the inventory market. As market situations evolve, your funding portfolio will look completely different at numerous factors within the 12 months. Portfolio rebalancing is a superb approach to make sure your funding allocation stays inside your threat tolerance stage. This tactic additionally helps you promote excessive and purchase low to maximise your wealth, and it could possibly open up alternatives to spend money on among the wealth-preserving tax-advantaged accounts we’ll go over under.

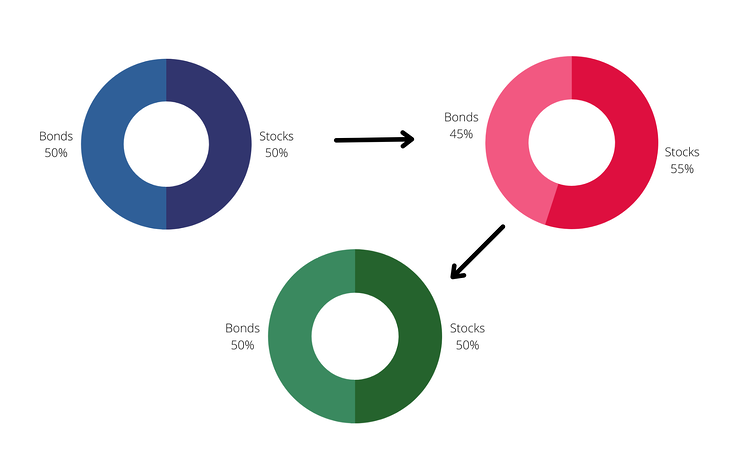

For instance, for those who make investments 50% of your portfolio within the inventory market and the opposite 50% in bonds, then shares go up by 10%, your portfolio might be out of stability and now not comprise a 50/50 cut up. As an alternative, you’ll now have 55% publicity to the inventory market, and your portfolio might be invested in a extra aggressive method than it was earlier than.

On this case, for those who had a rebalancing philosophy to comply with, it will information your subsequent transfer: Seize the chance to promote 5% of your shares at a excessive value, rebalance your portfolio (because you solely want 50% invested within the inventory market) and purchase into safer belongings to take some threat off the desk.

Need to create a monetary plan that helps you save as a lot as attainable at tax time? Schedule a name with a Bay Level Wealth advisor immediately to get began.

5 Tax-Environment friendly Funding Accounts To Contemplate When Rebalancing

You all the time need to take taxes into consideration when rebalancing. It’s essential to rebalance in a approach that preserves your wealth—however you understand that’s simpler stated than performed, particularly in relation to taxes. A method to economize that doesn’t require you to continuously observe your bills is through the use of tax-efficient investments.

A tax-efficient strategy helps decrease the quantity of tax you pay in your financial savings and investments, and it’s an integral a part of your monetary plan. Crucial factor to recollect about tax-efficient investments is that there are lots of choices, and a few could also be extra suited to your state of affairs than others—so be considerate about the place you’re placing your cash. (Tweet this!)

1. Employer-Matched 401(ok)

Many employers present this sort of retirement plan, which allows you to contribute a portion of your pre- or post-tax earnings. Your employer will then match a certain quantity of your contributions (the nationwide common is barely over 4%).

One vital advantage of a 401(ok) plan is which you could make investments a larger quantity of your earnings into this account than you possibly can put into a person retirement account (IRA) or a Roth IRA, which we’ll discover under. Individuals within the workforce below 50 years outdated might contribute as much as $22,500 per 12 months to their 401(ok), whereas these over 50 might put an extra $6,500 into their account yearly.

At minimal you must contribute the quantity that’s matched by your employer—it’s free cash!

2. Particular person Retirement Account (IRA)

In case your employer doesn’t supply a 401(ok) plan, an IRA is without doubt one of the most tax environment friendly funding accounts you possibly can select. This sort of account means that you can take a deduction in your contribution (so long as you meet sure earnings restrictions) and defer tax on the cash you initially deposit.

Your IRA can maintain shares and bonds. It’s a terrific match in case your tax fee is prone to be larger while you fund the account than it is going to be while you make a withdrawal—which is while you’ll be taxed in your earlier contributions. You should start taking cash out of your IRA while you attain age 73, however you can begin as early as age 59 for those who like.

3. Roth IRA

A Roth IRA is an account that permits your investments to develop tax-free. In distinction to a standard IRA, you pay tax upfront while you spend money on this sort of account. You’ll notice the advantages of a Roth IRA later down the highway while you need to withdraw your cash, since you received’t pay tax on it at the moment. That is particularly useful for those who’re in the next tax bracket while you withdraw the funds than you have been while you opened the account. For those who’re contemplating this sort of account, remember that Roth IRAs have numerous earnings limits.

4. Well being Financial savings Account (HSA)

You probably have a medical insurance plan with a excessive deductible, you’re eligible to open an HSA. People can put as much as $3,850 into their HSA, whereas households can contribute as much as $7,750 for 2023. The catch right here is that the cash should be used for medical bills or Medicare premiums. The principle advantage of an HSA is that any cash you’re taking out is tax-free.

Professional tip: Many individuals spend money on their HSA, let the wealth within the account develop till retirement, and use the cash then to cowl medical bills and Medicare premiums (HSA accounts are usually not allowed for use for medical insurance premiums). You obtain a tax deduction up entrance and the cash comes out tax-free, for use for medical bills or Medicare premiums. These 50 and older can contribute an extra $1,000.

5. 529 Account

A 529 account is without doubt one of the most tax-efficient investments obtainable for those who’re planning to avoid wasting up in your youngsters’s schooling or switch wealth to future generations.

Just like a Roth IRA, this sort of account grows tax-free. Nevertheless, a 529 account does not carry an annual contribution restrict, although it is really helpful you comply with the annual present tax limits. In distinction, in 2023 a Roth IRA solely means that you can put $6,500 into the account annually (or $7,500 for those who’re over 50). For those who’re saving for faculty, you’ll have a bigger window to extend your wealth than for those who’re saving for elementary or secondary faculty. 529 contributions are nonetheless owned by the Account Holder and could be accessed if wanted. As well as, you possibly can change beneficiaries if one (or extra) of your youngsters select to not go to school, or obtain a scholarship.

Rebalance Your Investments in Tax-Favored Accounts

It’s smart to decide on a number of kinds of tax-efficient accounts to broaden your portfolio, typically often called tax-diversification, and as a greatest apply it might even be prudent to you to incorporate completely different sorts of investments in every account. This technique is also known as asset location. For instance, it’s a good suggestion to maintain common bonds (which carry the next rate of interest) in your IRA to defer tax on these investments. However, in Roth IRAs and taxable accounts, it’s a good suggestion to spend money on extra shares, ETFs, mutual funds, and probably dividend-paying shares to seize as a lot tax-free progress as attainable.

Professional Tip: In a taxable account, shoot for extra progress as a result of capital positive factors—when realized—are taxed at a decrease fee than odd earnings.

Asset location has an impact on rebalancing. Throughout rebalancing, you’ll need to take into account and modify to the asset sorts in your portfolio. If, for instance, your portfolio is in a taxable account, there are tax implications every time you rebalance: You’ll set off capital positive factors while you promote and purchase. Contemplate which kinds of investments are fitted to which kinds of accounts—and which kinds of accounts name for sure rebalancing schedules.

Giving to charity is one other option to diversify your portfolio and decrease the quantity you owe in your tax return. For instance, for those who’re a enterprise proprietor and also you promote your organization for $1 million then resolve to present $100,000 to charity, you possibly can take your entire charitable tax deduction within the 12 months you promote the enterprise, however you don’t have to decide on the place to donate the cash till later. Utilizing a donor-advised fund means that you can make investments the cash and select the charity sooner or later.

Get Recommendation On Rebalancing With Taxes In Thoughts

Bay Level Wealth advisors transcend shopping for and promoting mutual funds. We attempt to discover alternatives that will help you get monetary savings and notice larger worth out of your investments. We will advocate probably the most tax-efficient investments in your private monetary state of affairs, and advise you on one of the best time to rebalance and reevaluate.

For those who’re serious about studying extra about rebalancing or tax-efficient investments, schedule a free session name with one in all our knowledgeable advisors immediately.